aleatory.processes.fBM#

- class aleatory.processes.fBM(hurst=0.5, T=1.0, rng=None)[source]#

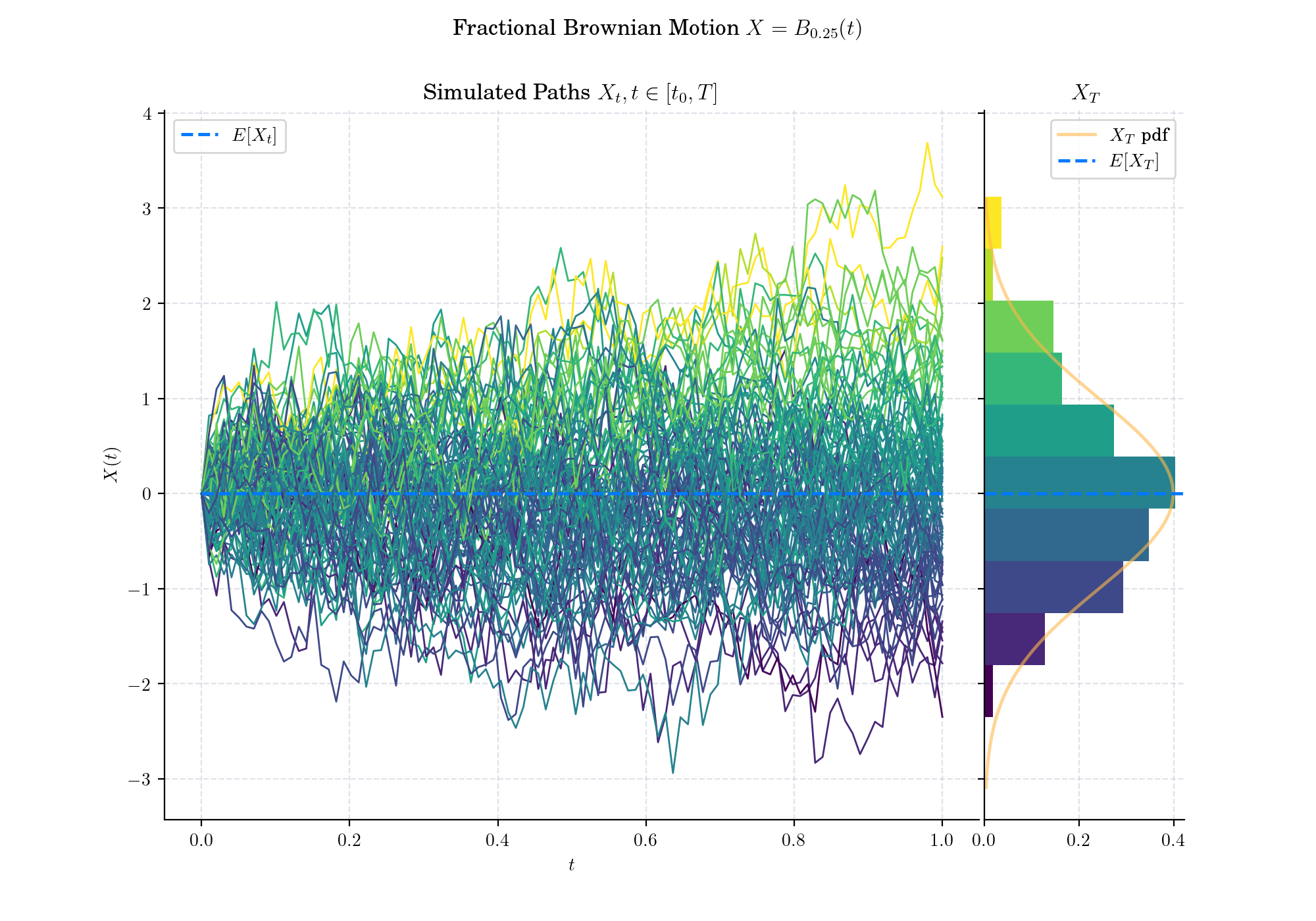

Fractional Brownian motion#

Notes#

A fractional Brownian motion (fBM) is a continuous-time Gaussian process \(B_H(t)\) on \([0,T]\) that starts at zero, has expectation zero for all \(t \in [0,T]\) and has the following covariance function:

\[E\left[B_H(t) B_H(s) \right] = \frac{1}{2}(|t|^{2H}+ |s|^{2H}- |t-s|^{2H}),\]where \(H\) is a real number in (0,1), called the Hurst or Hurst parameter.

Constructor, Methods, and Attributes#

- __init__(hurst=0.5, T=1.0, rng=None)[source]#

- Parameters:

hurst (float) – the Hurst parameter

T (float) – the right hand endpoint of the time interval \([0,T]\) for the process

rng (numpy.random.Generator) – a custom random number generator

Methods

__init__([hurst, T, rng])- parameter float hurst:

the Hurst parameter

draw(n, N[, T, marginal, envelope, title, ...])Simulates and plots paths/trajectories from the instanced stochastic process.

estimate_covariances([times])estimate_expectations()estimate_quantiles(q)estimate_stds()estimate_variances()get_marginal(t)marginal_expectation([times])marginal_stds([times])marginal_variance([times])plot(n, N[, T, title, suptitle])Simulates and plots paths/trajectories from the instanced stochastic process.

plot_covariance([times, title])plot_kernel([times, colormap, matrix_shape, ...])plot_kernel3d([times, title])plot_mean_variance([times, title])plot_paths_and_kernel(n, N[, T, title, ...])Plots the paths of the process and the covariance kernel.

process_covariance([times])process_expectation()process_stds()process_variance()sample(n)simulate(n, N[, T])Simulate paths/trajectories from the instanced stochastic process.

Attributes

TEnd time of the process.

rng