aleatory.processes.BrownianMotion#

- class aleatory.processes.BrownianMotion(drift=0.0, scale=1.0, initial=0.0, T=1.0, rng=None)[source]#

Brownian Motion#

A one-dimensional standard Brownian motion object.

Notes#

A standard Brownian motion \(\{W_t : t \geq 0\}\) is defined by the following properties:

Starts at zero, i.e. \(W(0) = 0\)

Independent increments

\(W(t) - W(s)\) follows a Gaussian distribution \(N(0, t-s)\)

Almost surely continuous

A more general version of a Brownian motion, is the Arithmetic Brownian Motion which is defined by the following SDE

\[dX_t = \mu dt + \sigma dW_t \ \ \ \ t\in (0,T]\]with initial condition \(X_0 = x_0\in\mathbb{R}\), where

\(\mu\) is the drift

\(\sigma>0\) is the volatility

\(W_t\) is a standard Brownian Motion

Clearly, the solution to this equation can be written as

\[X_t = x_0 + \mu t + \sigma W_t \ \ \ \ t \in [0,T]\]and each \(X_t \sim N(\mu t, \sigma^2 t)\).

Examples#

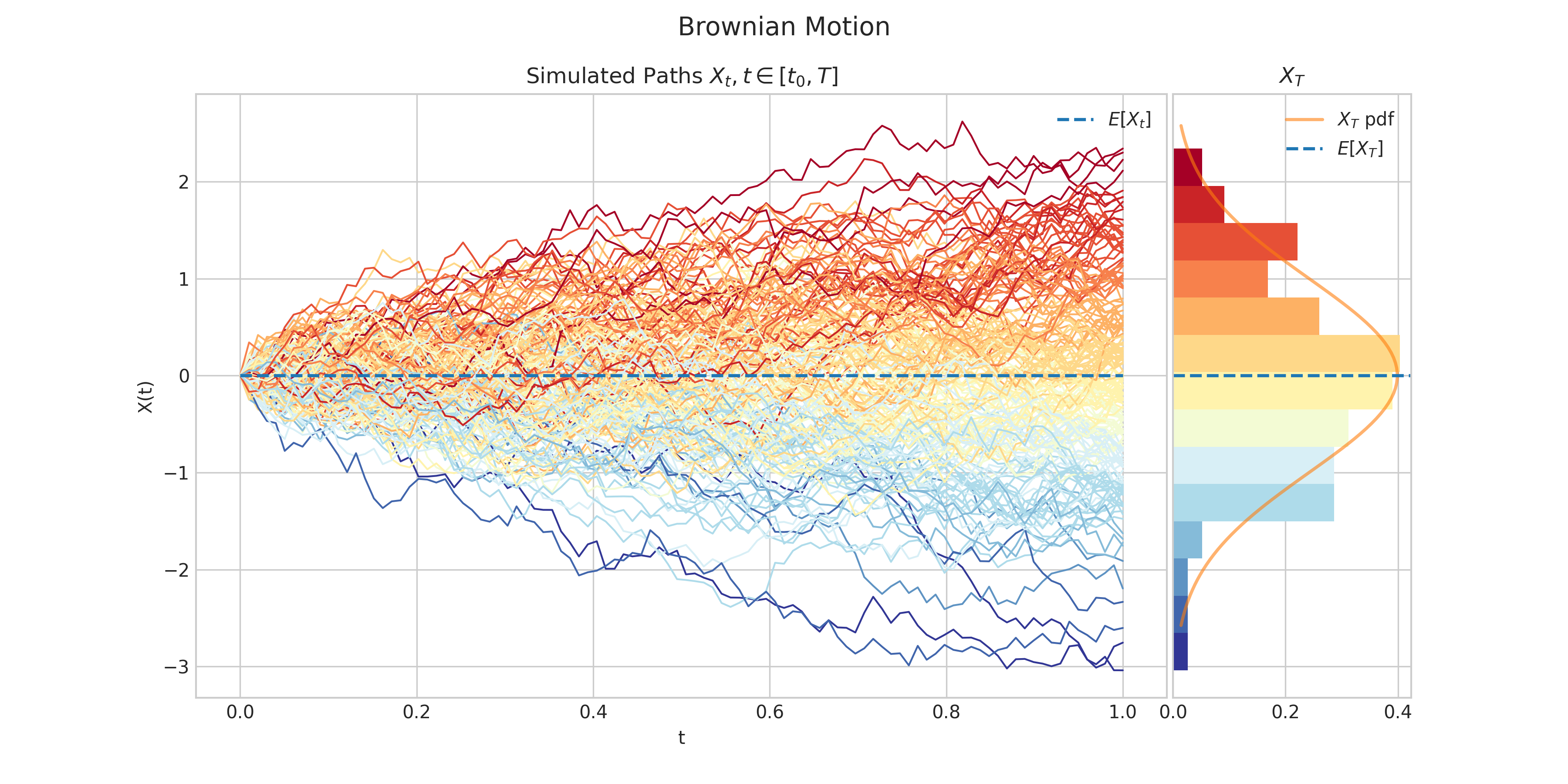

from aleatory.processes import BrownianMotion process = BrownianMotion() fig = process.plot(n=100, N=5, figsize=(12, 7)) fig.show()

from aleatory.processes import BrownianMotion process = BrownianMotion() fig = process.draw(n=100, N=100, figsize=(12, 7)) fig.show()

Constructor, Methods, and Attributes#

- __init__(drift=0.0, scale=1.0, initial=0.0, T=1.0, rng=None)[source]#

- Parameters:

drift (double) – the drift parameter \(\mu\) in the above SDE

scale (double) – the scale parameter \(\sigma\) in the above SDE

initial (double) – the initial condition \(x_0\) in the above SDE

T (double) – the endpoint of the time interval \([0,T]\) over which the process is defined

rng – random number generator for reproducibility

Methods

__init__([drift, scale, initial, T, rng])- param double drift:

the drift parameter \(\mu\) in the above SDE

draw(n, N[, T, marginal, envelope, type, title])Simulates and plots paths/trajectories from the instanced stochastic process.

estimate_covariances([times])estimate_expectations()estimate_quantiles(q)estimate_stds()estimate_variances()get_marginal(t)marginal_expectation([times])marginal_stds([times])marginal_variance(times)plot(n, N[, T, title, suptitle])Simulates and plots paths/trajectories from the instanced stochastic process.

plot_covariance([times, title])plot_kernel([times, colormap, matrix_shape, ...])plot_kernel3d([times, title])plot_mean_variance(times, **fig_kw)plot_paths_and_kernel(n, N[, T, title, ...])Plots the paths of the process and the covariance kernel.

process_covariance([times])process_expectation()process_stds()process_variance()sample(n)Generates a discrete time sample from a Brownian Motion instance.

sample_at(times)Generates a sample from a Brownian motion at the specified times.

simulate(n, N[, T])Simulate paths/trajectories from the instanced stochastic process.

Attributes

TEnd time of the process.

driftinitialrngscale