aleatory.processes.GammaProcess#

- class aleatory.processes.GammaProcess(mu=1.0, nu=1.0, T=10.0, rng=None)[source]#

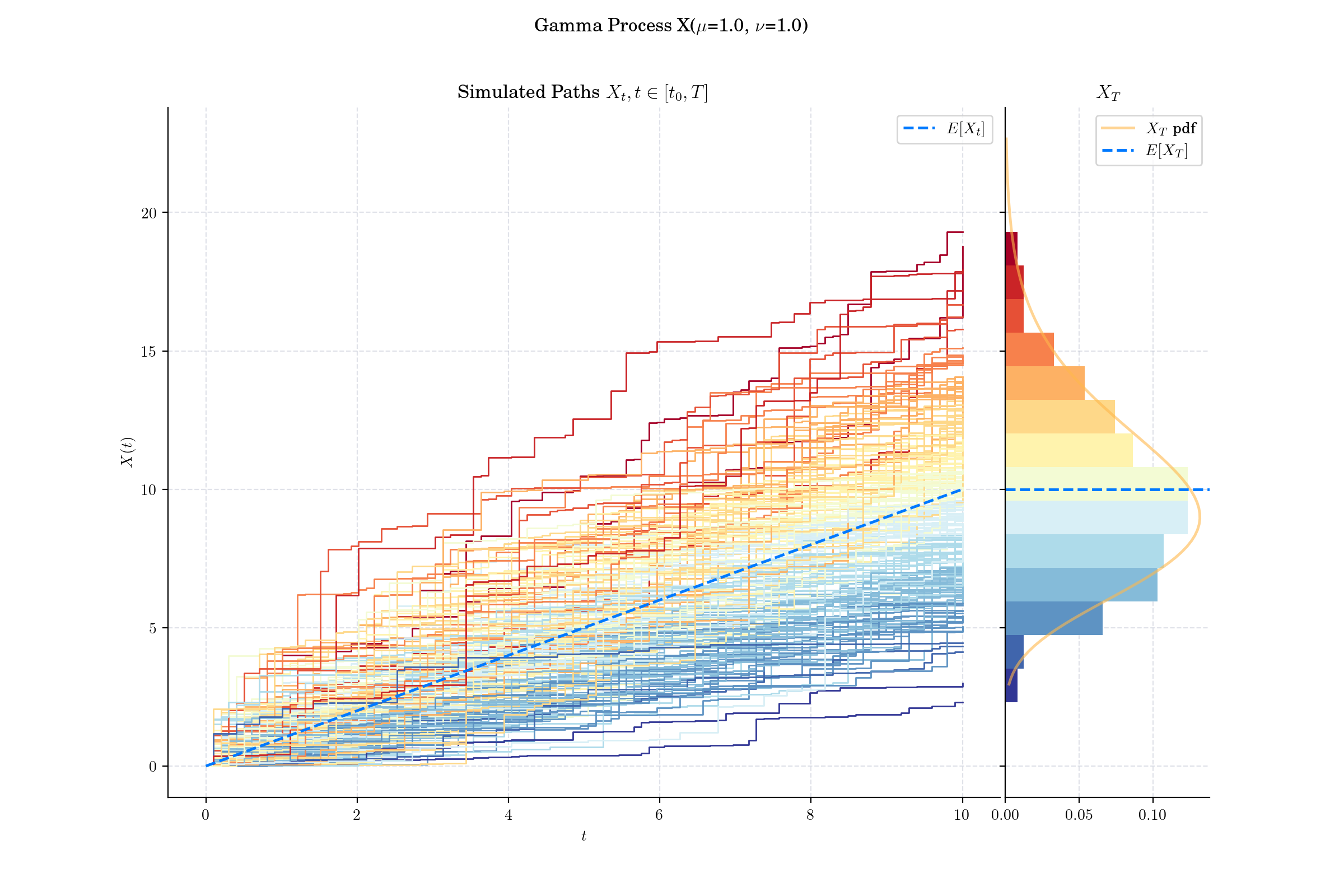

Gamma process#

Notes#

The gamma process \(X = \{ X(t; \mu,\nu) : t \geq 0\}\) with mean parameter \(\mu\) and variance parameter \(\nu\) is a continuous-time process with stationary, independent increments such that

\[X(t + h; \mu, \nu)− X(t; \mu, \nu) \sim Gamma\left( \frac{\mu^2 h}{\nu}, \frac{\nu}{\mu} \right),\]for any \(h > 0\).

Constructor, Methods, and Attributes#

- __init__(mu=1.0, nu=1.0, T=10.0, rng=None)[source]#

- Parameters:

mu (float) – the parameter \(\mu\) in the above definition

nu (float) – the parameter \(\nu\) in the above definition

Methods

__init__([mu, nu, T, rng])- parameter float mu:

the parameter \(\mu\) in the above definition

draw(n, N[, T, marginal, envelope, mode, title])Simulates and plots paths/trajectories from the instanced stochastic process.

estimate_covariances([times])estimate_expectations()estimate_quantiles(q)estimate_stds()estimate_variances()get_marginal(t)marginal_expectation([times])marginal_stds([times])marginal_variance([times])plot(n, N[, T, mode, title])Simulates and plots paths/trajectories from the instanced stochastic process.

plot_covariance([times, title])plot_kernel([times, colormap, matrix_shape, ...])plot_kernel3d([times, title])plot_mean_variance([times, title])plot_paths_and_kernel(n, N[, T, title, ...])Plots the paths of the process and the covariance kernel.

process_covariance([times])process_expectation()process_stds()process_variance()sample(n)Generates a discrete time sample from a Gamma process instance.

sample_at(times)Generates a sample from a Gamma process at the specified times.

simulate(n, N[, T])Simulate paths/trajectories from the instanced stochastic process.

Attributes

TEnd time of the process.

munurng