aleatory.processes.CIRProcess#

- class aleatory.processes.CIRProcess(theta=1.0, mu=2.0, sigma=0.5, initial=5.0, T=1.0, rng=None)[source]#

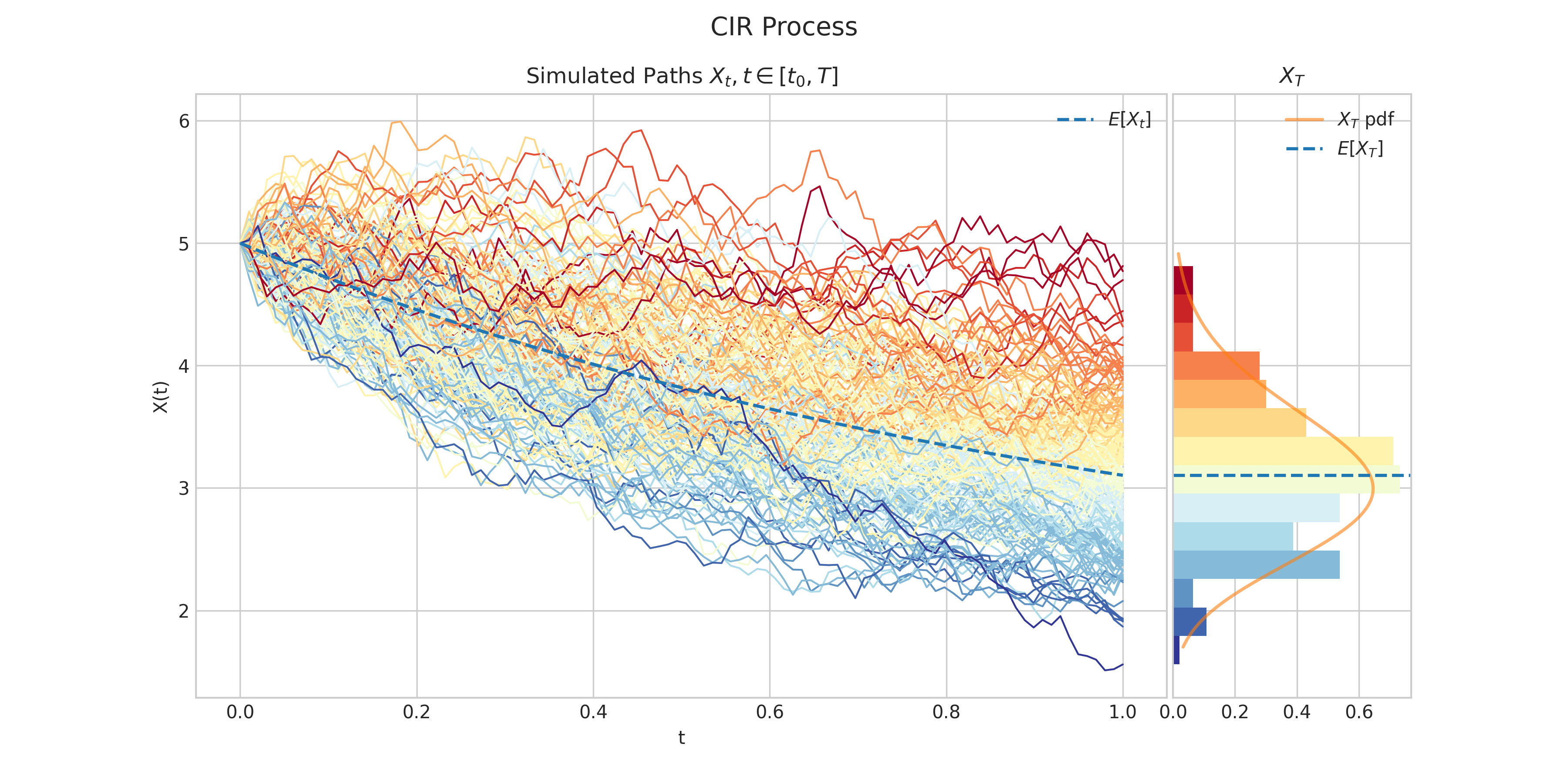

Cox–Ingersoll–Ross (CIR) Process#

Notes#

A Cox–Ingersoll–Ross process \(X = \{X : t \geq 0\}\) is characterised by the following Stochastic Differential Equation

\[dX_t = \theta(\mu - X_t) dt + \sigma \sqrt{X_t} dW_t, \ \ \ \ \forall t\in (0,T],\]with initial condition \(X_0 = x_0\), where

\(\theta\) is the rate of mean reversion

\(\mu\) is the long term mean value.

\(\sigma>0\) is the instantaneous volatility

\(W_t\) is a standard Brownian Motion.

It can be seen that each \(X_t\) follows a non-central chi-square distribution.

Constructor, Methods, and Attributes#

- __init__(theta=1.0, mu=2.0, sigma=0.5, initial=5.0, T=1.0, rng=None)[source]#

- Parameters:

theta (float) – the parameter \(\theta\) in the above SDE

mu (float) – the parameter \(\mu\) in the above SDE

sigma (float) – the parameter \(\sigma>0\) in the above SDE

initial (float) – the initial condition \(x_0\) in the above SDE

T (float) – the right hand endpoint of the time interval \([0,T]\) for the process

rng (numpy.random.Generator) – a custom random number generator

Methods

__init__([theta, mu, sigma, initial, T, rng])- param float theta:

the parameter \(\theta\) in the above SDE

draw(n, N[, T, marginal, envelope, title, ...])Simulates and plots paths/trajectories from the instanced stochastic process.

estimate_covariances([times])estimate_expectations()estimate_quantiles(q)estimate_stds()estimate_variances()get_marginal(t)marginal_df()marginal_expectation([times])marginal_nc_parameter([times])marginal_scale([times])marginal_stds([times])marginal_variance([times])plot(n, N[, T, title, suptitle])Simulates and plots paths/trajectories from the instanced stochastic process.

plot_covariance([times, title])plot_kernel([times, colormap, matrix_shape, ...])plot_kernel3d([times, title])plot_mean_variance([times, title])plot_paths_and_kernel(n, N[, T, title, ...])Plots the paths of the process and the covariance kernel.

process_covariance([times])process_expectation()process_stds()process_variance()sample(n)simulate(n, N[, T])Simulate paths/trajectories from the instanced stochastic process.

Attributes

TEnd time of the process.

murngsigmatheta