Analytical Processes#

The aleatory.processes module provides classes for continuous-time stochastic processes which can be expressed in

analytical form.

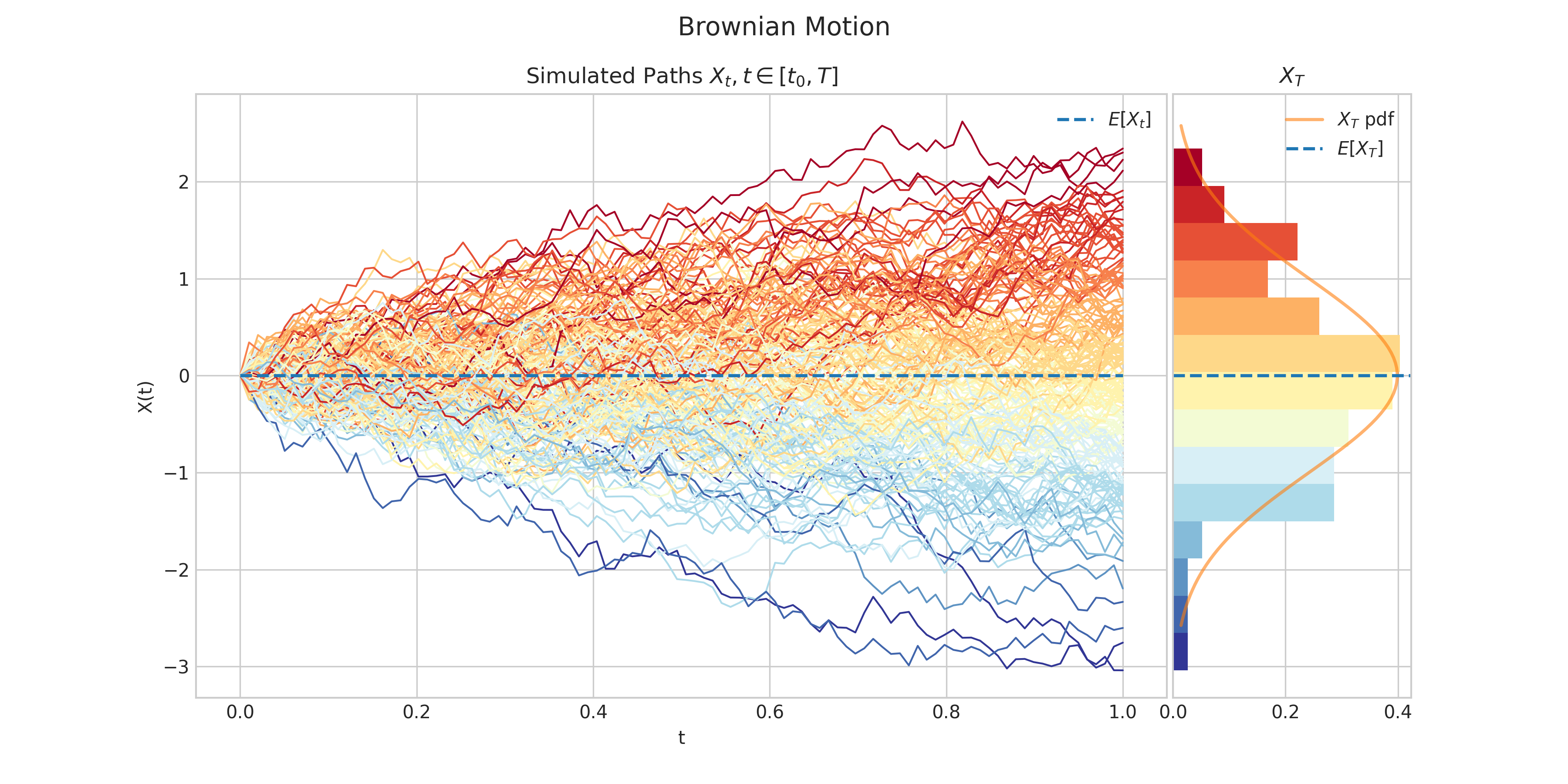

- class aleatory.processes.BrownianMotion(drift=0.0, scale=1.0, T=1.0, rng=None)[source]#

Brownian motion

A standard Brownian motion \(\{W_t : t \geq 0\}\) is defined by the following properties:

Starts at zero, i.e. \(W(0) = 0\)

Independent increments

\(W(t) - W(s)\) follows a Gaussian distribution \(N(0, t-s)\)

Almost surely continuous

A more general version of a Brownian motion, is the Drifted Brownian Motion which is defined by the following SDE

\[dX_t = \mu dt + \sigma dW_t \ \ \ \ t\in (0,T]\]with initial condition \(X_0 = x_0\in\mathbb{R}\), where

\(\mu\) is the drift

\(\sigma>0\) is the volatility

\(W_t\) is a standard Brownian Motion.

Clearly, the solution to this equation can be written as

\[X_t = x_0 + \mu t + \sigma W_t \ \ \ \ t \in [0,T]\]and each \(X_t \sim N(\mu t, \sigma^2 t)\).

Parameters:

- Parameters:

drift (float) – the parameter \(\mu\) in the above SDE

scale (float) – the parameter \(\sigma>0\) in the above SDE

initial (float) – the initial condition \(x_0\) in the above SDE

T (float) – the right hand endpoint of the time interval \([0,T]\) for the process

rng (numpy.random.Generator) – a custom random number generator

- property T#

End time of the process.

- draw(n, N, marginal=True, envelope=False, type='3sigma', title=None, **fig_kw)[source]#

Simulates and plots paths/trajectories from the instanced stochastic process.

Produces different kind of visualisation illustrating the following elements:

times versus process values as lines

the expectation of the process across time

histogram showing the empirical marginal distribution \(X_T\) (optional when

marginal = True)probability density function of the marginal distribution \(X_T\) (optional when

marginal = True)envelope of confidence intervals across time (optional when

envelope = True)

- Parameters:

n – number of steps in each path

N – number of paths to simulate

marginal – bool, default: True

envelope – bool, default: False

type – string, default: ‘3sigma’

title – string to customise plot title

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

- sample(n)[source]#

Generates a discrete time sample from a Brownian Motion instance.

- Parameters:

n – the number of steps

- Returns:

numpy array

- sample_at(times)[source]#

Generates a sample from a Brownian motion at the specified times.

- Parameters:

times – the times which define the sample

- Returns:

numpy array

- simulate(n, N)#

Simulate paths/trajectories from the instanced stochastic process.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

- Returns:

list with N paths (each one is a numpy array of size n)

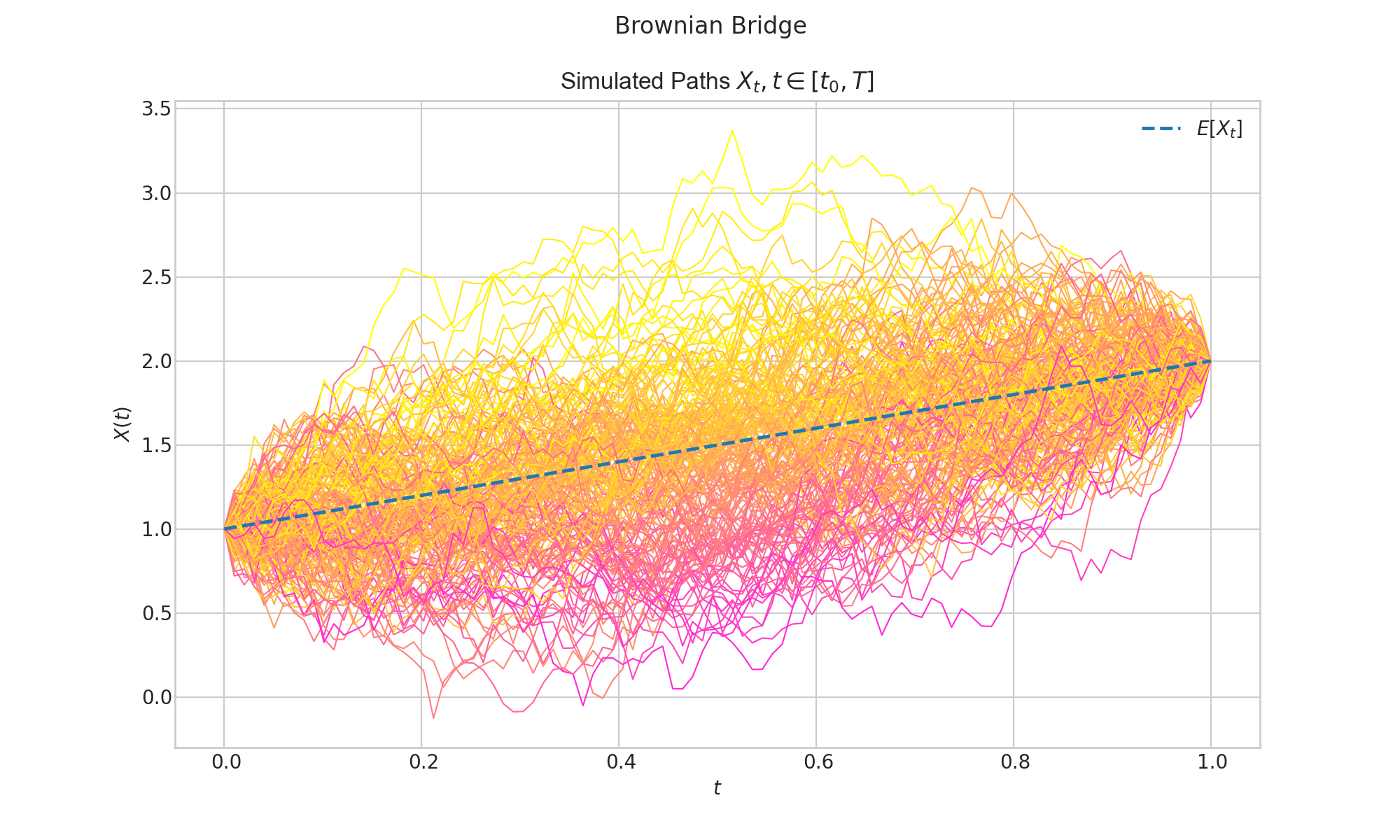

- class aleatory.processes.BrownianBridge(initial=0.0, end=0.0, T=1.0, rng=None)[source]#

Brownian Bridge

A Brownian bridge is a continuous-time stochastic process \(\{B_t : t \geq 0\}\) whose probability distribution is the conditional probability distribution of a standard Wiener process (Brownian Motion) \(\{W_t : t \geq 0\}\) subject to the condition that \(W(T) = 0\), so that the process is pinned to the same value at both \(t = 0\) and \(t = T\). More specifically,

\[B_t = (W_t | W_T = 0), \ \ \ \ t\in (0,T].\]More generally, a Brownian Bridge is subject to the conditions \(W(0) = a\) and \(W(T) = b\).

- Parameters

- param float initial:

initial condition

- param float end:

end condition

- param float T:

the right hand endpoint of the time interval \([0,T]\)

for the process :param numpy.random.Generator rng: a custom random number generator

- property T#

End time of the process.

- draw(n, N, envelope=False, title=None, **fig_kw)[source]#

Simulates and plots paths/trajectories from the instanced stochastic process.

Produces different kind of visualisation illustrating the following elements:

times versus process values as lines

the expectation of the process across time

envelope of confidence intervals across time (optional when

envelope = True)

- Parameters:

n – number of steps in each path

N – number of paths to simulate

envelope – bool, default: False

title – string to customise plot title

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

- sample(n)[source]#

Generates a discrete time sample from a Brownian Motion instance.

- Parameters:

n – the number of steps

- Returns:

numpy array

- sample_at(times)[source]#

Generates a sample from a Brownian motion at the specified times.

- Parameters:

times – the times which define the sample

- Returns:

numpy array

- simulate(n, N)#

Simulate paths/trajectories from the instanced stochastic process.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

- Returns:

list with N paths (each one is a numpy array of size n)

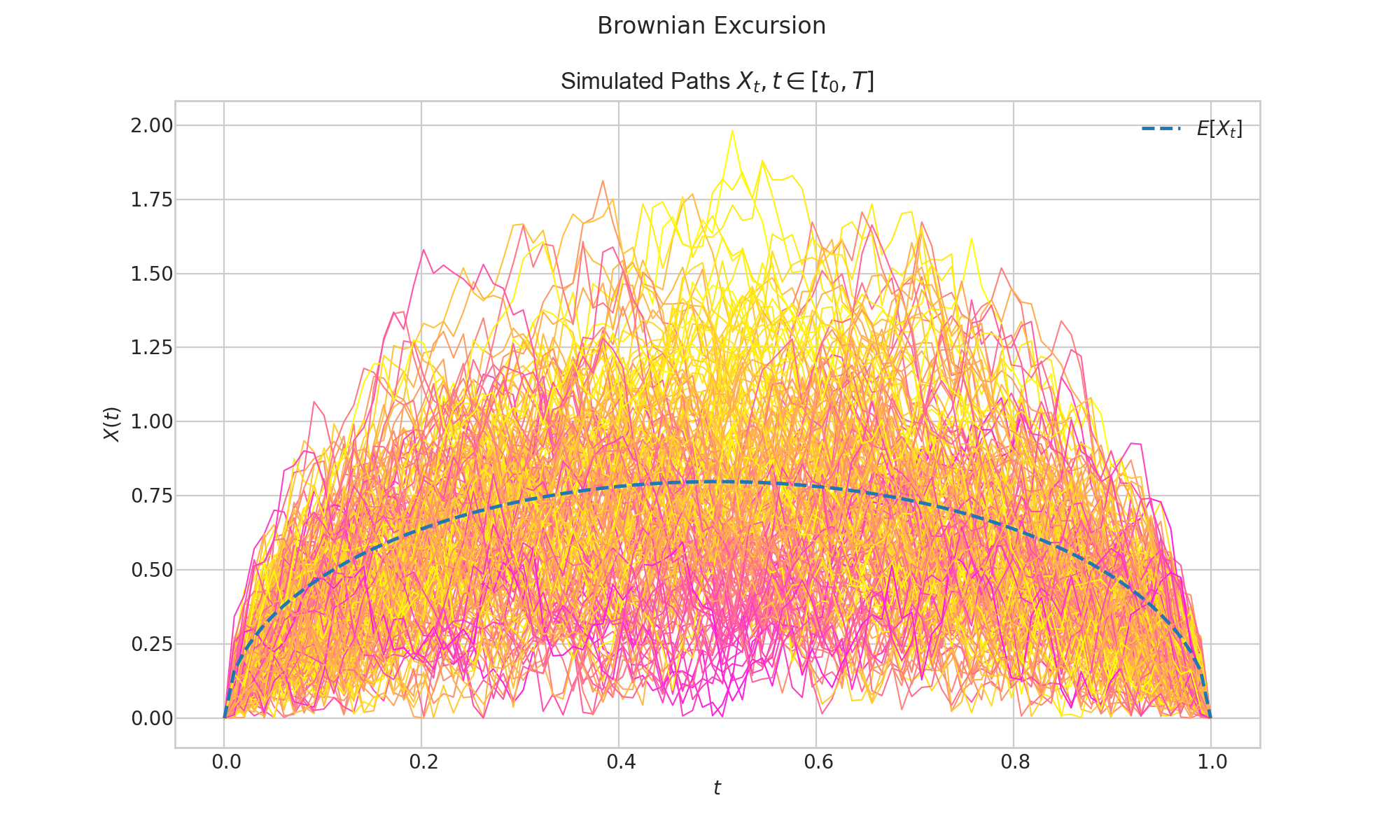

- class aleatory.processes.BrownianExcursion(T=1.0, rng=None)[source]#

Brownian Excursion

A Brownian excursion process, is a Wiener process (or Brownian motion) conditioned to be positive and to take the value 0 at time 1. Alternatively, it can be defined as a Brownian Bridge process conditioned to be positive.

- Parameters

- param float T:

the right hand endpoint of the time interval \([0,T]\)

for the process :param numpy.random.Generator rng: a custom random number generator

- property T#

End time of the process.

- draw(n, N, envelope=False, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process.

Produces different kind of visualisation illustrating the following elements:

times versus process values as lines

the expectation of the process across time

envelope of confidence intervals across time (optional when

envelope = True)

- Parameters:

n – number of steps in each path

N – number of paths to simulate

envelope – bool, default: False

title – string to customise plot title

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

- sample(n)[source]#

Generates a discrete time sample from a Brownian Motion instance.

- Parameters:

n – the number of steps

- Returns:

numpy array

- sample_at(times)[source]#

Generates a sample from a Brownian motion at the specified times.

- Parameters:

times – the times which define the sample

- Returns:

numpy array

- simulate(n, N)#

Simulate paths/trajectories from the instanced stochastic process.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

- Returns:

list with N paths (each one is a numpy array of size n)

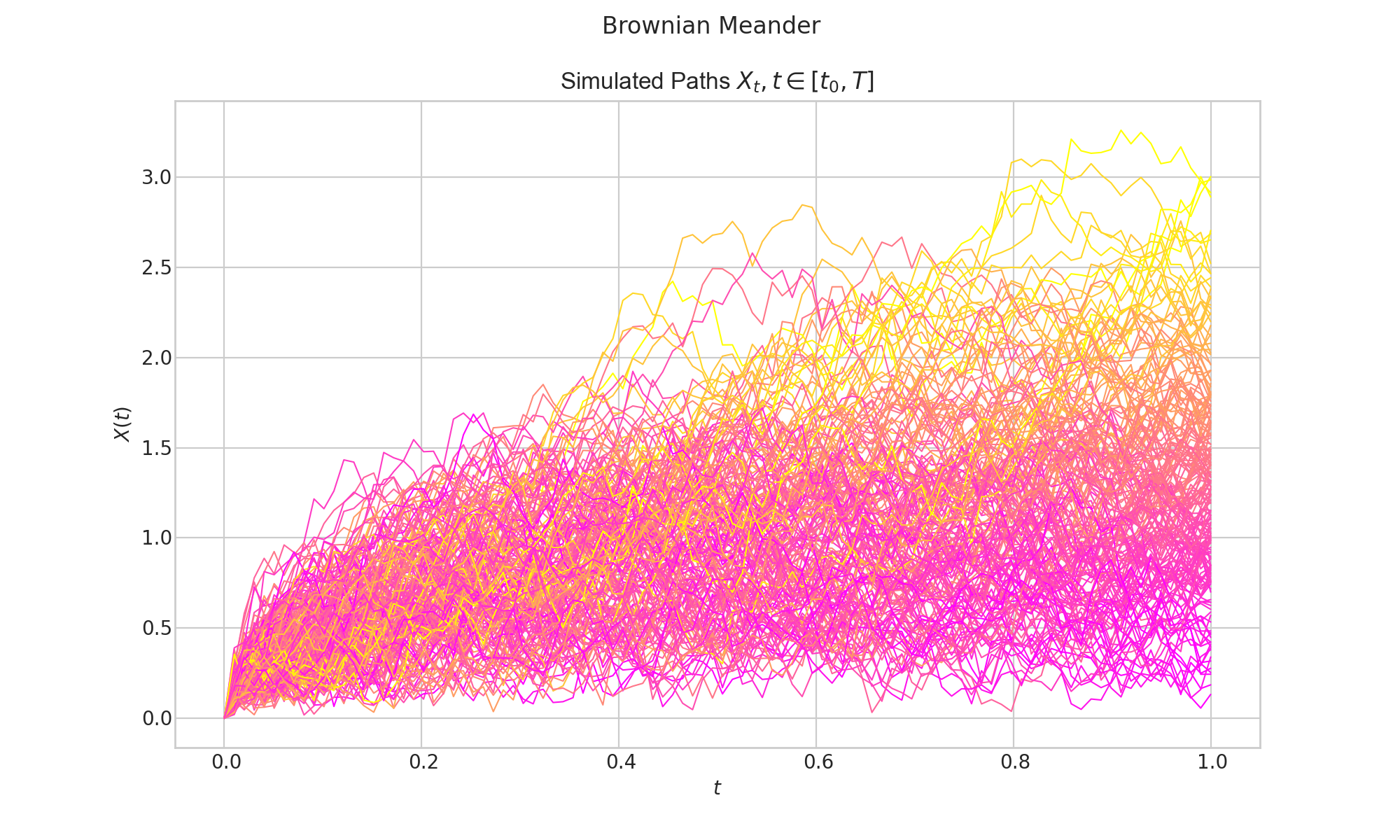

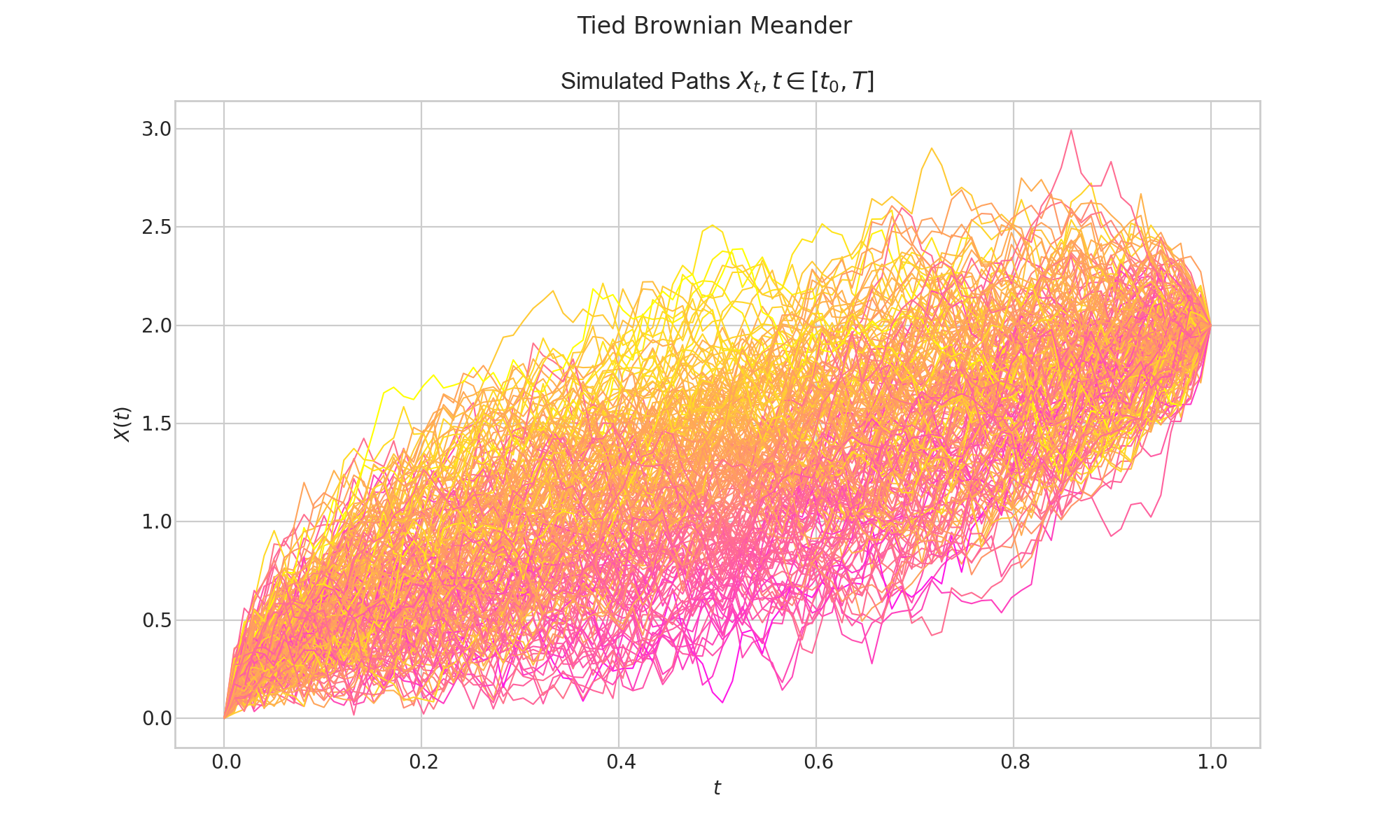

- class aleatory.processes.BrownianMeander(T=1.0, fixed_end=False, end=None, rng=None)[source]#

Brownian Meander

Let \(\{W_t : t \geq 0\}\) be a standard Brownian motion and

\[\tau = \sup\{ t \in [0,1] : W_t =0\},\]i.e. the last time before t = 1 when \(W_t\) visits zero. Then the Brownian Meander is defined as follows

\[W_t^{+} = \frac{1}{\sqrt{1-\tau}} |W(\tau + t (1-\tau))|, \ \ \ \ t\in (0,1].\]Parameters

- property T#

End time of the process.

- draw(n, N, title=None, **fig_kw)[source]#

Simulates and plots paths/trajectories from the instanced stochastic process.

Produces different kind of visualisation illustrating the following elements:

times versus process values as lines

the expectation of the process across time

histogram showing the empirical marginal distribution \(X_T\) (optional when

marginal = True)probability density function of the marginal distribution \(X_T\) (optional when

marginal = True)envelope of confidence intervals across time (optional when

envelope = True)

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

- sample(n)[source]#

Generates a discrete time sample from a Brownian Motion instance.

- Parameters:

n – the number of steps

- Returns:

numpy array

- sample_at(times)[source]#

Generates a sample from a Brownian motion at the specified times.

- Parameters:

times – the times which define the sample

- Returns:

numpy array

- simulate(n, N)#

Simulate paths/trajectories from the instanced stochastic process.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

- Returns:

list with N paths (each one is a numpy array of size n)

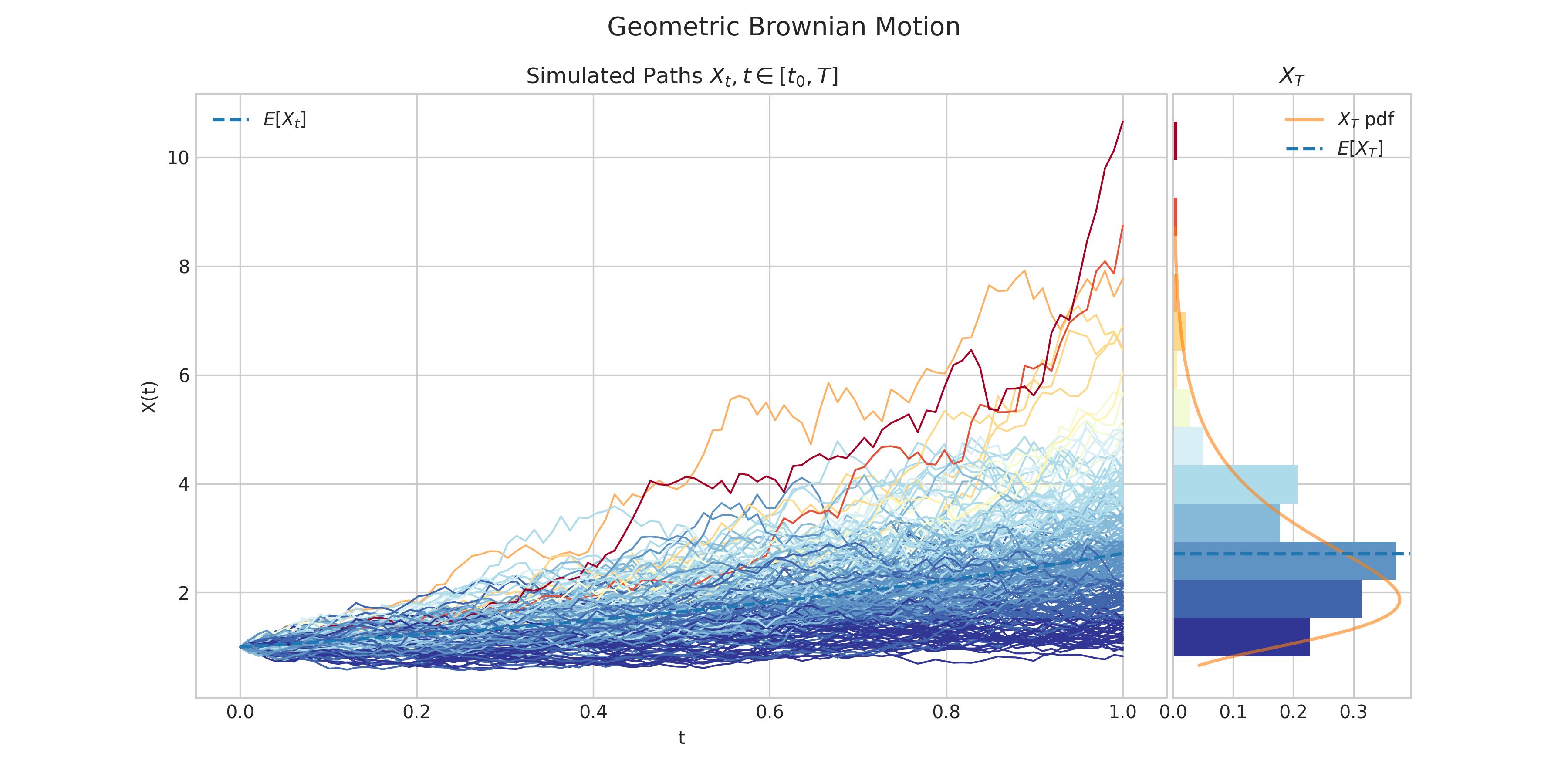

- class aleatory.processes.GBM(drift=1.0, volatility=0.5, initial=1.0, T=1.0, rng=None)[source]#

Geometric Brownian Motion

A Geometric Brownian Motion \(\{X(t) : t \geq 0\}\) is characterised by the following SDE.

\[dX_t = \mu X_t dt + \sigma X_t dW_t \ \ \ \ t\in (0,T]\]with initial condition \(X_0 = x_0\geq0\), where

\(\mu\) is the drift

\(\sigma>0\) is the volatility

\(W_t\) is a standard Brownian Motion.

The solution to this equation can be written as

\[X_t = x_0\exp\left((\mu + \frac{\sigma^2}{2} )t +\sigma W_t\right)\]and each \(X_t\) follows a log-normal distribution.

- Parameters:

drift (float) – the parameter \(\mu\) in the above SDE

volatility (float) – the parameter \(\sigma>0\) in the above SDE

initial (float) – the initial condition \(x_0\) in the above SDE

T (float) – the right hand endpoint of the time interval \([0,T]\) for the process

rng (numpy.random.Generator) – a custom random number generator

- property T#

End time of the process.

- draw(n, N, marginal=True, envelope=False, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Visualisation shows - times versus process values as lines - the expectation of the process across time - histogram showing the empirical marginal distribution \(X_T\) - probability density function of the marginal distribution \(X_T\) - envelope of confidence intervals

- Parameters:

n – number of steps in each path

N – number of paths to simulate

marginal – bool, default: True

envelope – bool, default: False

title – string optional default to None

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

- simulate(n, N)#

Simulate paths/trajectories from the instanced stochastic process.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

- Returns:

list with N paths (each one is a numpy array of size n)

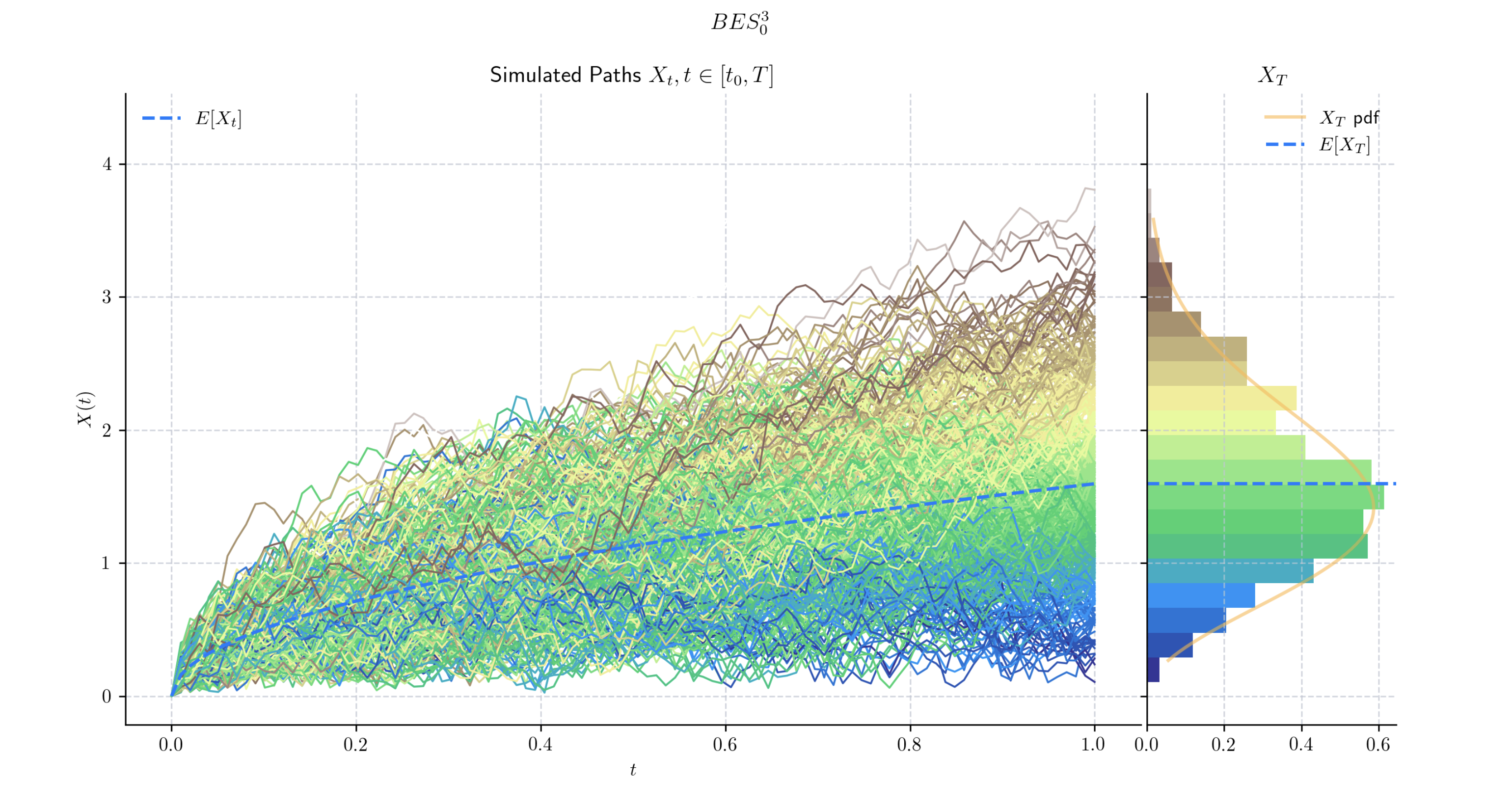

- class aleatory.processes.BESProcess(dim=1.0, initial=0.0, T=1.0, rng=None)[source]#

Bessel process

A Bessel process \(BES^{n}_{0},\) for \(n\geq 2\) integer is a continuous stochastic process \(\{X(t) : t \geq 0\}\) characterised as the Euclidian norm of an \(n\)-dimensional Brownian motion. That is,

\[X_t = \sqrt{\sum_{i=1}^n (W^i_t)^2}.\]More generally, for any \(\delta >0\), and \(x_0 \geq 0\), a Bessel process of dimension \(\delta\) starting at \(x_0\), denoted by

\[BES_{{x_0}}^{{\delta}}\]can be defined by the following SDE

\[dX_t = \frac{(\delta-1)}{2} \frac{dt}{X_t} + dW_t \ \ \ \ t\in (0,T]\]with initial condition \(X_0 = x_0\geq 0.\), where

\(\delta\) is a positive real

\(W_t\) is a standard one-dimensional Brownian Motion.

- Parameters:

dim (double) – the dimension of the process \(n\)

initial (double) – the initial point of the process \(x_0\)

T (double) – the right hand endpoint of the time interval \([0,T]\) for the process

rng (numpy.random.Generator) – a custom random number generator

- property T#

End time of the process.

- draw(n, N, marginal=True, envelope=False, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Visualisation shows - times versus process values as lines - the expectation of the process across time - histogram showing the empirical marginal distribution \(X_T\) - probability density function of the marginal distribution \(X_T\) - envelope of confidence intervals

- Parameters:

n – number of steps in each path

N – number of paths to simulate

marginal – bool, default: True

envelope – bool, default: False

title – string optional default to None

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns:

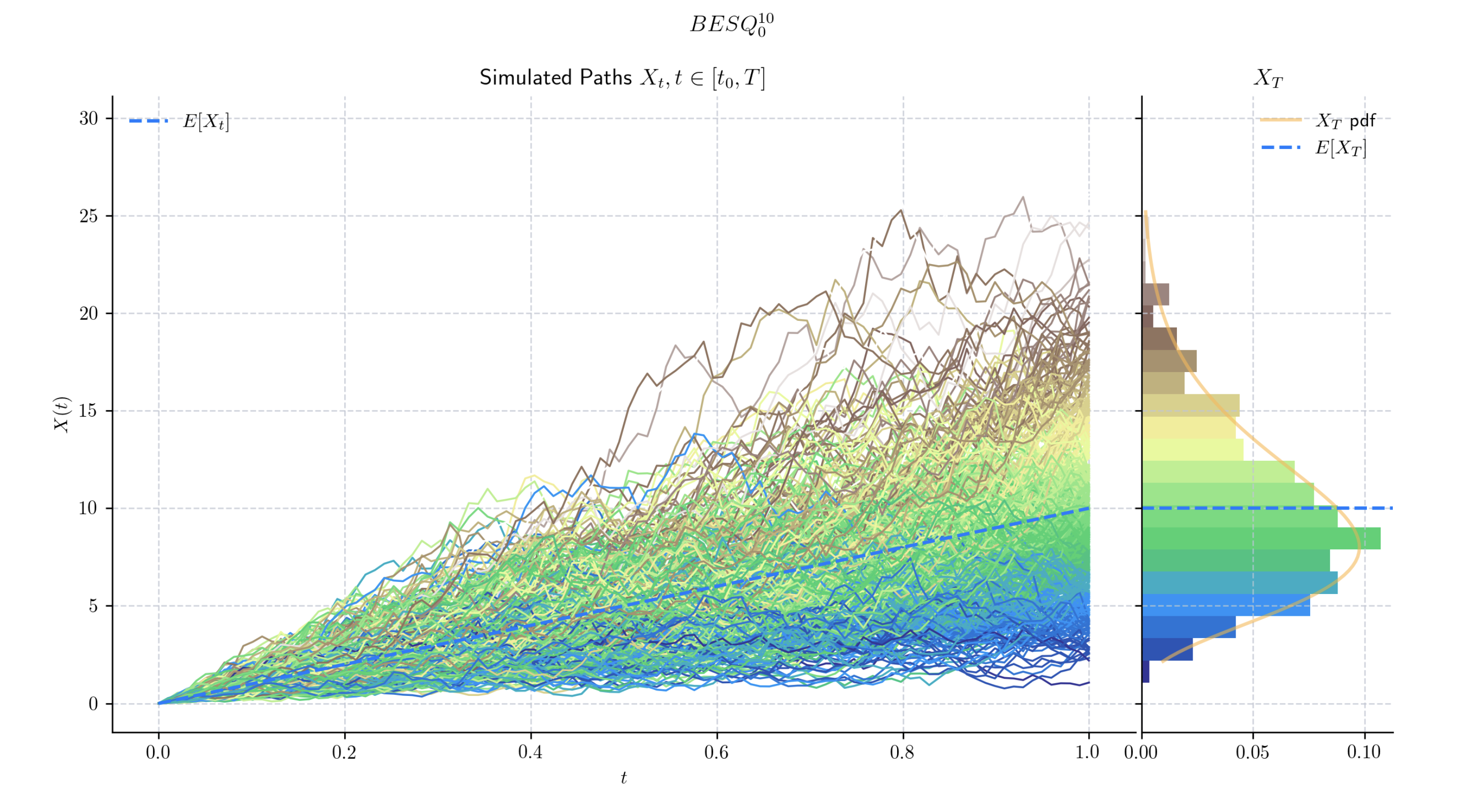

- class aleatory.processes.BESQProcess(dim=1.0, initial=0.0, T=1.0, rng=None)[source]#

Squared Bessel process

A squared Bessel process \(BESQ^{n}_{0}\), for \(n\) integer is a continuous stochastic process \(\{X(t) : t \geq 0\}\) which is characterised as the squared Euclidian norm of an \(n\)-dimensional Brownian motion. That is,

\[X_t = \sum_{i=1}^n (W^i_t)^2.\]More generally, for any \(\delta >0\), and \(x_0 \geq 0\), a squared Bessel process of dimension \(\delta\) starting at \(x_0\), denoted by

\[BESQ_{{x_0}}^{{\delta}}\]can be defined by the following SDE

\[dX_t = \delta dt + 2\sqrt{X_t} dW_t \ \ \ \ t\in (0,T]\]with initial condition \(X_0 = x_0\), where

\(\delta\) is a positive real

\(W_t\) is a standard Brownian Motion.

- Parameters:

dim (double) – the dimension of the process \(n\)

initial (double) – the initial point of the process \(x_0\)

T (double) – the right hand endpoint of the time interval \([0,T]\) for the process

rng (numpy.random.Generator) – a custom random number generator

- property T#

End time of the process.

- draw(n, N, marginal=True, envelope=False, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Visualisation shows - times versus process values as lines - the expectation of the process across time - histogram showing the empirical marginal distribution \(X_T\) - probability density function of the marginal distribution \(X_T\) - envelope of confidence intervals

- Parameters:

n – number of steps in each path

N – number of paths to simulate

marginal – bool, default: True

envelope – bool, default: False

title – string optional default to None

- Returns:

- plot(n, N, title=None, **fig_kw)#

Simulates and plots paths/trajectories from the instanced stochastic process. Simple plot of times versus process values as lines and/or markers.

- Parameters:

n – number of steps in each path

N – number of paths to simulate

title – string to customise plot title

- Returns: